We start by taking a comprehensive look at your assets, income stream, and future anticipated expenses. Applying the asset-liability matching strategy, we formulate a plan, staggering maturity dates as soon as three months and up to 30 years. However, since the world changes dynamically, we seek to maintain flexibility, usually sticking with fixed-income investments weighted more heavily in the short- to medium-term so we can adapt and avoid incurring undesirable inflation risk through overexposure to long-term bonds.

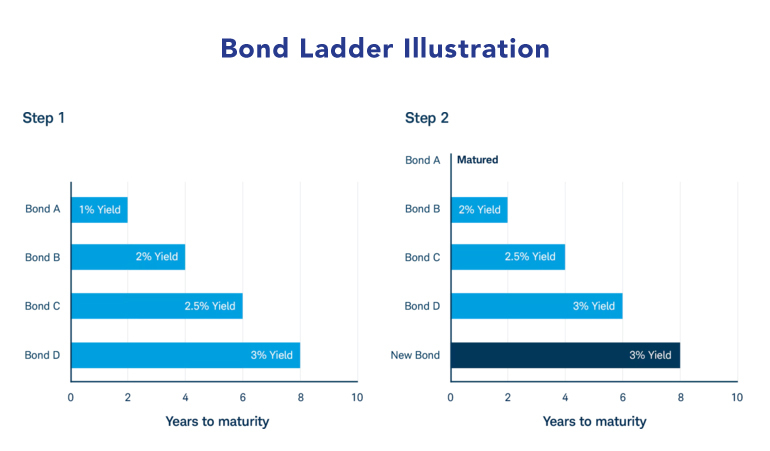

Using a bond ladder strategy, an investor buys several bonds with staggered maturities. Once bond A matures, the investor reinvests the proceeds into a new bond, extending the ladder.

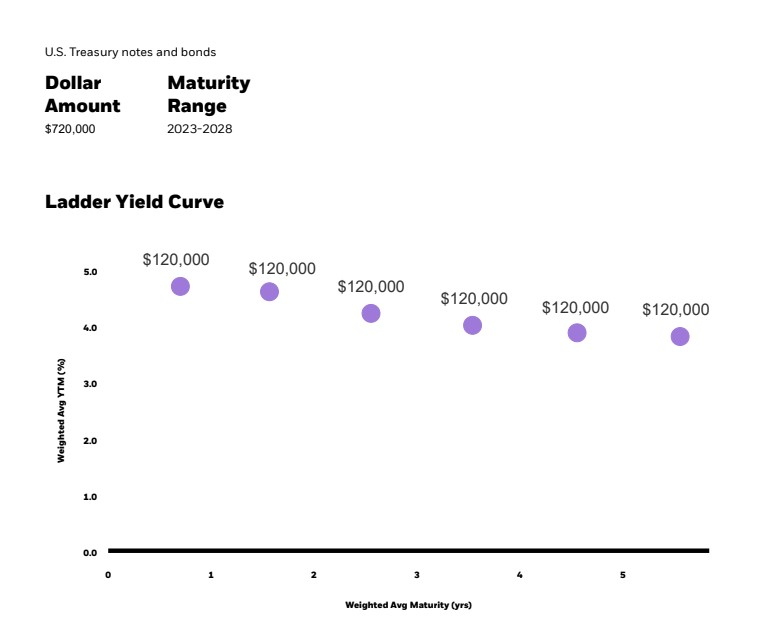

Source: Charles Schwab

Our process seeks to manage inflation risk by selecting shorter maturities to ensure we don’t tie up funds for too long, thus hedging inflation. This approach allows for regular revaluation in conjunction with all the components in our Retirement Decision Dashboard.

U.S. Treasury Bonds and Notes Ladder Yield Curve

The longer the overall duration of a bond portfolio, the more exposure to the risk of higher-than-expected future long-term inflation.

As near-term bonds mature, our clients can choose to use the proceeds to fund their retirement spending, rebalance into stocks, or roll them into higher rates at the end of the ladder if rates have risen. This strategy helps capture higher yields in a rising rate environment compared to an aggregate longer-term bond fund by mitigating risk when interest rates rise while providing a steady cash flow as some portion of the retirement portfolio matures each year as planned.

In conclusion

Feeling confident and secure in your retirement portfolio is challenging but achievable. By implementing the asset-liability matching strategy and considering inflation, credit, and interest rate risks, incorporating low-risk shorter-term Treasury Bonds into your overall portfolio emerges as a highly reliable choice. Laddering bond maturities effectively serves as an insurance policy, ensuring predictable income streams while mitigating risk during volatile times.

Toberman Becker Wealth is a fee-only, independent fiduciary firm based in St. Louis. Whether starting to invest for retirement in your 50s or actively planning for retirement in your 60s, we help people nearing a transition build a resilient retirement plan. We operate in the best interests of our clients, always, and our top priority is to help you live comfortably now, without compromising your financial future later.

If you’re looking for an investment advisor to help you craft a diversified strategy that safeguards against risk, feel free to book a meeting or give us a call.

Craig Toberman is a Partner at Toberman Becker Wealth – a fee-only, fiduciary financial advisor based in St. Louis. He assists families and businesses with strategic financial planning and long-term wealth management. He has over a decade of experience in financial services and has crafted custom financial plans for hundreds of families and businesses.