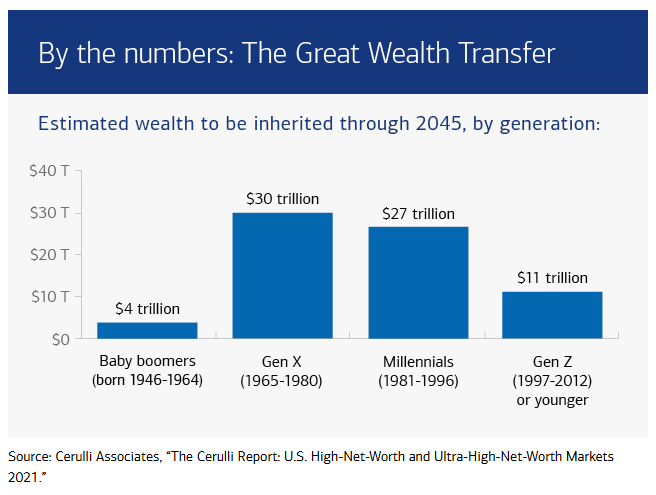

What Is the “Great Wealth Transfer” & Who Does It Affect?

The Great Wealth Transfer refers to an estimated $84 Trillion in assets that will pass from Baby Boomers to younger generations, including:

- Generation X | Born 1965-1980

- Millennials | Born 1981-1996

- Generation Z | Born after 1996

Will the Great Wealth Transfer Lead to Financial Windfall?

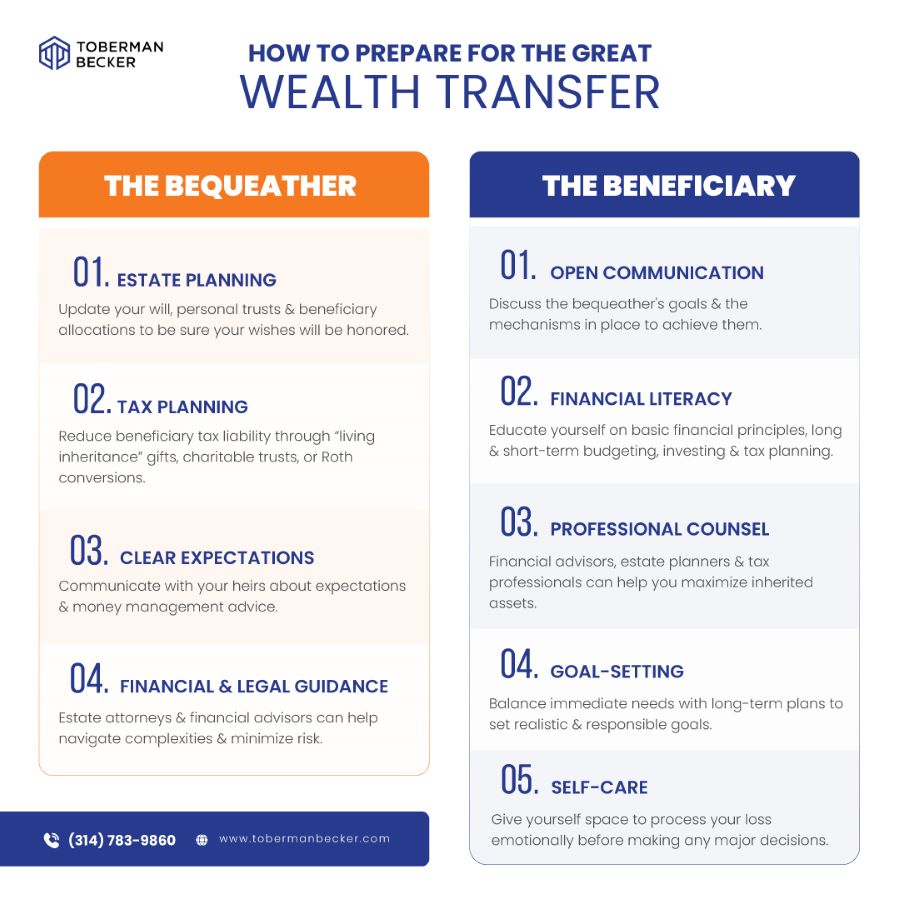

Though individuals with wealthy parents or grandparents in the Boomer generation are likely to inherit significant assets during the Great Wealth Transfer, a financial windfall is not guaranteed for all.

Factors such as taxes, outstanding debts, philanthropic endowments, or multiple heirs can diminish the extent of an individual’s inheritance. Additionally, wills and estate plans contain highly personal and often unpredictable decisions made with full autonomy by the deceased.

Michael is a highly knowledgeable and experienced partner at Toberman Becker Wealth in St. Louis. With his expertise in investment management, behavioral finance, and retirement planning, Michael is dedicated to providing his clients with the best financial guidance possible.

Having worked with clients on complex estate planning and developing investment strategies for a team of advisors, Michael’s experience spans across various areas of financial planning. What truly sets him apart is his unyielding desire to acquire knowledge for the betterment of his clients. At Toberman Becker Wealth, this commitment to continuous learning is the foundation upon which exceptional client experiences are built.

Michael earned a Bachelor of Science degree in Finance and Banking from the University of Missouri – Columbia. Additionally, he holds designations as a Chartered Financial Analyst (CFA) charterholder and Certified Financial Planner (CFP).

Beyond his professional achievements, Michael enjoys a fulfilling personal life in St. Louis. Living with his wife, Lindsey, and their beloved dog, Birk, he finds joy in activities such as golfing together and exploring local restaurants.