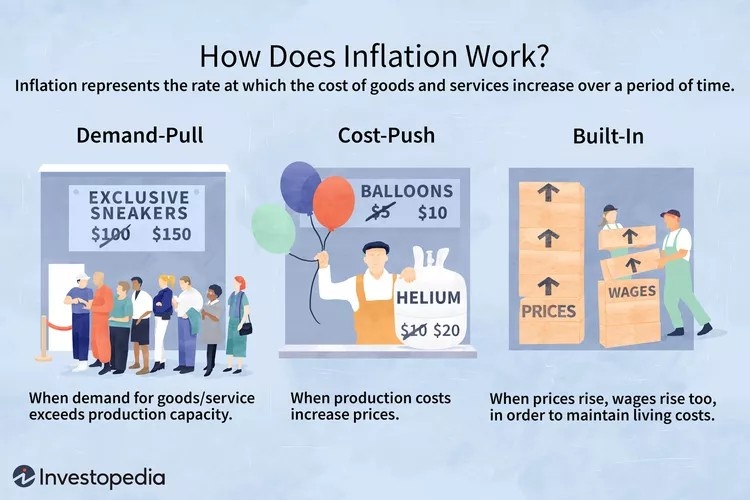

5 Strategies to Help Protect Your Retirement Investments From Inflation

While short-term inflation spikes can feel unsettling, proper planning can help keep your 30-year retirement on track. By adopting a risk-management mindset and building a holistic “insurance” framework, you can better protect your portfolio from inflation over the long term.

Here are five ways to minimize inflation’s impact on your retirement investments:

- Diversify Your Bond Portfolio

When you purchase a bond, you lend money to an issuer (government, municipality, or corporation), and in turn, the issuer promises to pay you a specific rate of interest during the life of the bond and repay you the principal when it “matures” or comes due after a set period of time.

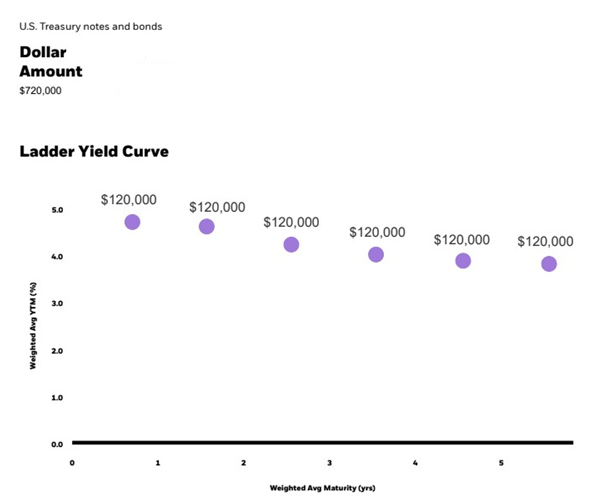

- Diversify Your Bond Portfolio

U.S. Treasury Bonds and Notes Ladder Yield Curve

Illustrates how a bond ladder helps reduce inflation-related risk by spreading

$720,000 across six equal Treasury investments with staggered maturity dates.

Bonds provide steady income, but inflation erodes the value of those future payments. To protect your bond holdings, diversify your portfolio by:

- Mixing short- and long-term bonds

Long-term bonds are more sensitive to inflation and rising rates. You can offset some of this inflationary risk by buying short-term bonds and reinvesting the principal. - Investing in Treasury Inflation-Protected Securities (TIPS)

TIPS are bonds that adjust with inflation. Though initial yields are lower, they offer valuable long-term protection. - Holding different bond types

Combine U.S. Treasury issues, Certificates of Deposit (CDs), and municipal bonds to reduce credit risk, and stagger maturity rates to lessen interest-rate risk.

- Mixing short- and long-term bonds

Bonds can provide a reliable retirement income; however, fixed-rate bonds alone may not provide enough growth. Complement them with assets that historically outpace inflation.

- Timing and Strategy Use smart investment timing strategies to manage inflation and market volatility.

- Be mindful of when to purchase

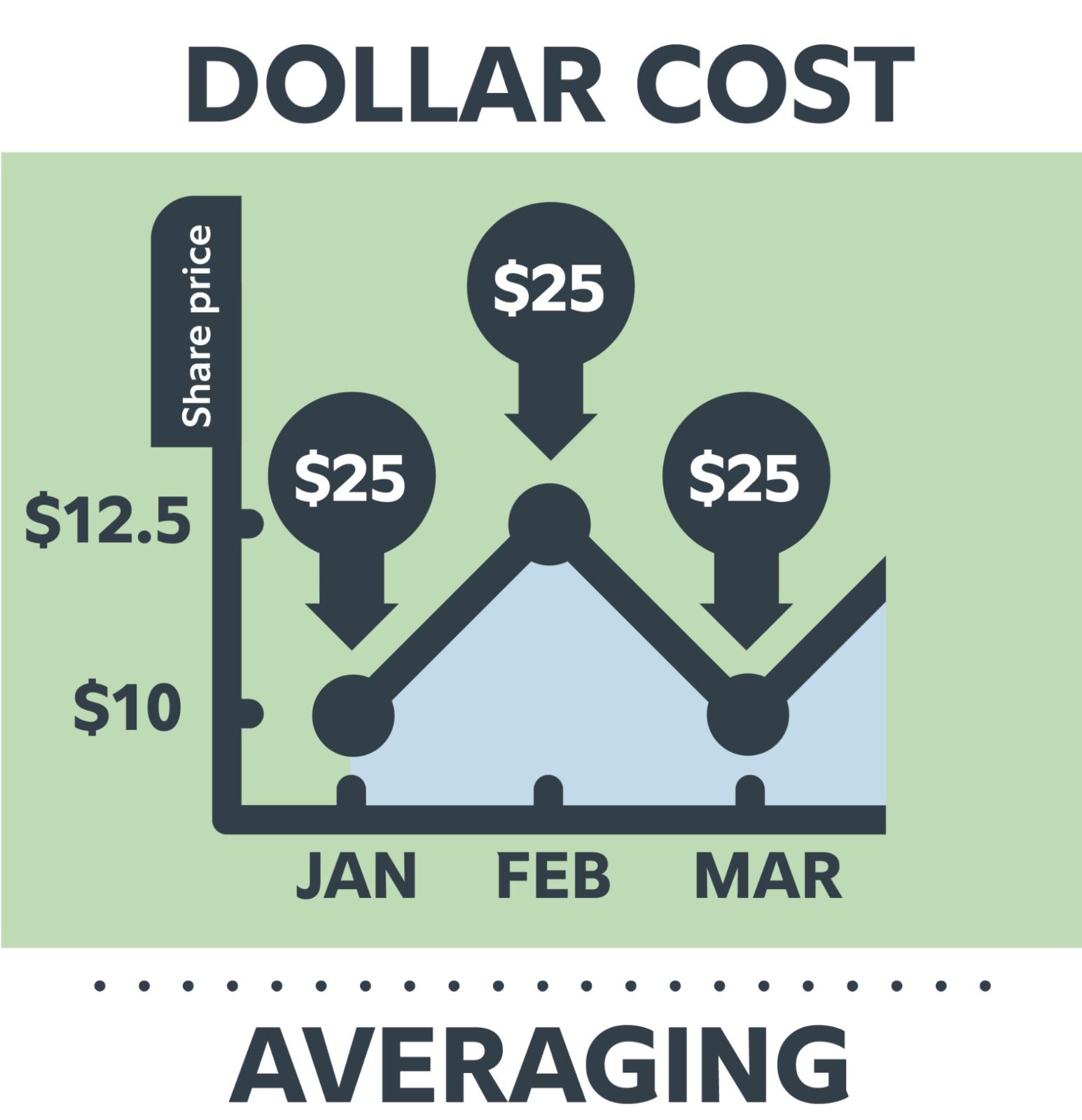

Whether you plan to let your bonds mature or sell them to make a profit, “ladder” your bond exposure (buy bonds that mature across a span of years) so you can reinvest income as they mature and diversify the interest-rate risk in your portfolio. - Consider dollar-cost averaging

Dollar-cost averaging is when you invest the same amount at regular intervals, regardless of market prices. This approach helps reduce market timing risk and keeps you consistently invested. - Rebalance for inflation protection

Monitor and adjust your portfolio periodically to keep your goals on track and hedge against inflation.

Shows the practice of investing the same amount in regular intervals,

regardless of the current market price

Source: Fidelity

Shows the practice of investing the same amount in regular intervals,

regardless of the current market price

Source: Fidelity

Craig Toberman is a Partner at Toberman Becker Wealth – a fee-only, fiduciary financial advisor based in St. Louis. He assists families and businesses with strategic financial planning and long-term wealth management. He has over a decade of experience in financial services and has crafted custom financial plans for hundreds of families and businesses.