1. Know Your Full Retirement Age and Estimated Benefit

Before you can make any decisions about Social Security, you need to know two numbers: your full retirement age and your estimated monthly benefit. These numbers are the foundation for every other strategy in this article.

Your full retirement age (FRA) is the age at which you’re entitled to 100% of the benefit you’ve earned. It depends on when you were born:

| Birth Year | Full Retirement Age | Reduction at 62 | Benefit at 70 (% of FRA) |

|---|---|---|---|

| 1943-1954 | 66 | 25% | 132% |

| 1955 | 66 and 2 months | 25.83% | 130.67% |

| 1956 | 66 and 4 months | 26.67% | 129.33% |

| 1957 | 66 and 6 months | 27.5% | 128% |

| 1958 | 66 and 8 months | 28.33% | 126.67% |

| 1959 | 66 and 10 months | 29.17% | 125.3% |

| 1960 or later | 67 | 30% | 124% |

Source: Social Security Administration

Your FRA matters because it’s the line between a reduced benefit and an increased one.

- You can claim as early as age 62, but doing so permanently lowers your monthly check by as much as roughly 30% if you claim the moment you’re eligible.

- Wait until you are FRA, and you receive your full benefit.

- Delay beyond FRA and you earn delayed retirement credits worth about 8% per year, up to age 70, after which there’s no additional gain from waiting.

To see your own numbers rather than general rules, create a free “my Social Security” account at SSA.gov. There you’ll find personalized benefit estimates at 62, at your FRA, and at 70, and you can confirm that your earnings record is accurate, which directly affects the benefit you’ll receive.

For early retirees, it’s especially important to understand that your estimates are based on your earnings to date and assume you continue to earn your current pay until the year you start your benefits.

Note: The figures above reflect current Social Security rules. Because these parameters can change, confirm the specifics for your situation at SSA.gov or with your advisor.

2. Work at Least 35 Years to Maximize Your Benefit

Your Social Security benefit is calculated based on your highest 35 years of earnings. If you report income for fewer than 35 years, zeros will be averaged into your calculation, drastically reducing your benefit amount.

- Track Your Earnings Record

Social Security statements are available online at SSA.gov. Review your record to verify the accuracy of your earnings history. - Consider a Part-Time Exit Strategy

If you’re eager to retire but have less than 35 years of earnings, even part-time income can boost your average and improve your benefit calculation by replacing zero-earning years.

3. Delay Your Social Security Claim to Maximize Monthly Benefits

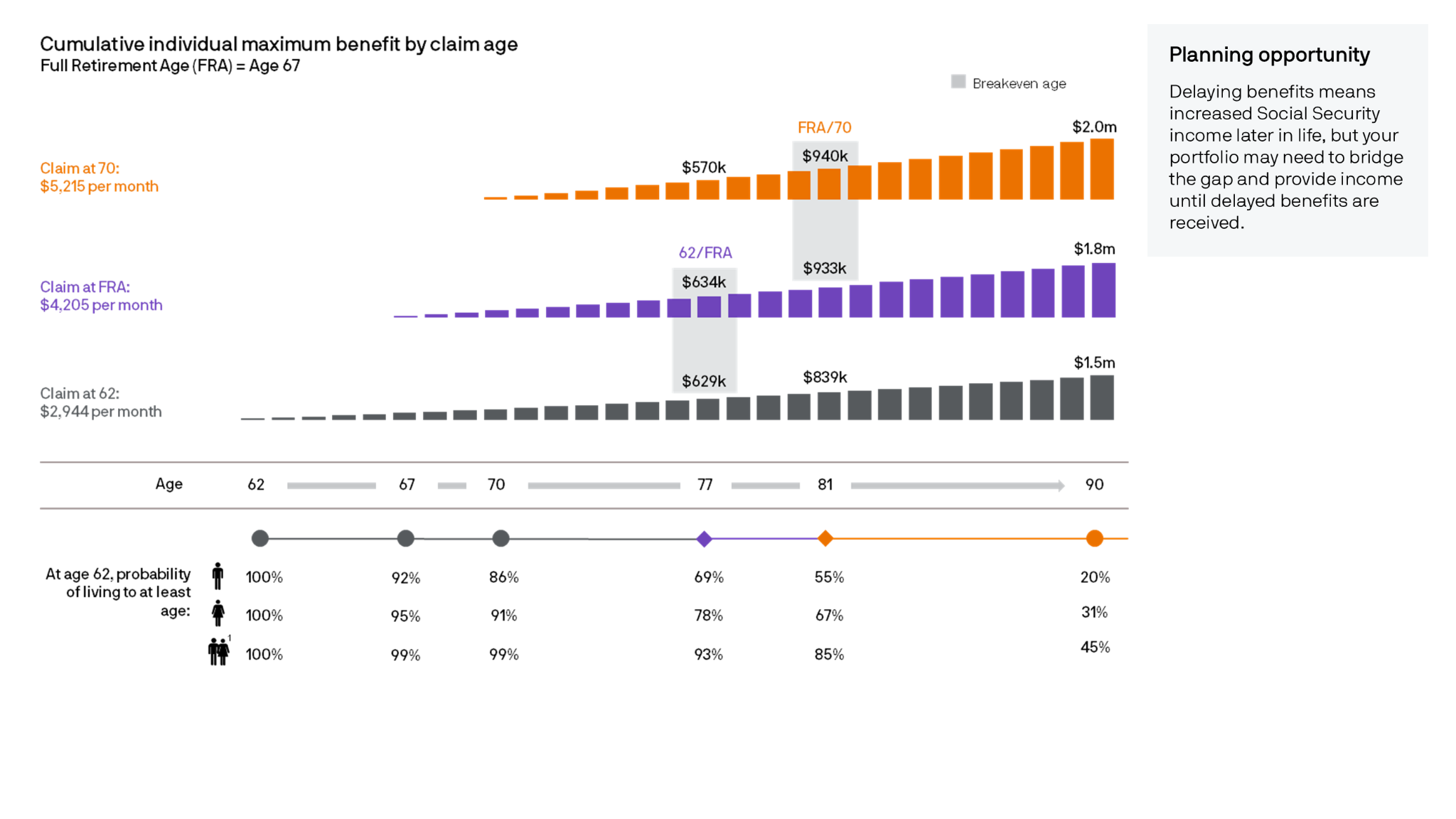

Retirees can start claiming benefits anytime between the ages of 62 and 70. Those who wait until 70 maximize their monthly check, receiving up to roughly 124% of their full benefit (for anyone with a full retirement age of 67).

The cumulative maximum benefit for an individual varies by claim age. An individual who claims benefits at Full Retirement Age will not break even with the delayed option until age 80.

Source: 2026 JP Morgan Guide to Retirement

Here are three options to consider, using a $3,000 full benefit as an example:

- Early Retirement | Ages 62-66

- Benefit reduction: Up to 30% lower benefits

- Sample benefit: $2,100/month

- Full Retirement Age (FRA) | Age 67

- Full benefit

- Sample benefit: $3,000/month

- Delayed | Ages 68-70

- Benefit increase: about 8% per year after FRA, up to a total 24% increase by age 70

- Sample benefit: $3,720/month

Claiming benefits at age 70 provides the highest possible monthly benefit. While the break-even age compared with claiming at age 67 is typically in the early 80s, individuals who live beyond that point can benefit from greater cumulative lifetime income and increased financial security throughout retirement.

Craig Toberman is a Partner at Toberman Becker Wealth – a fee-only, fiduciary financial advisor based in St. Louis. He assists families and businesses with strategic financial planning and long-term wealth management. He has over a decade of experience in financial services and has crafted custom financial plans for hundreds of families and businesses.