What is a 401(k), and How Does It Differ from Other Retirement Savings Plans?

A 401(k) is an employer-sponsored retirement plan, meaning your company sets it up for you rather than you opening it yourself. This contrasts with individual retirement accounts (IRAs), which you open yourself through a financial institution.

Benefits of a 401(k) vs. an IRA Include:

- Payroll Deductions

Contributions come straight from your paycheck, providing automatic retirement savings accrual. - Higher Contribution Limits

2026 contribution limits range from $24,500 to $35,750, depending on age. This is significantly higher than IRA limits ($7,500 to $8,600). - Employer Contributions

Many employers provide 401(k) contributions as part of their benefits package, typically through a capped percentage match based on employee contributions. That’s free money toward your retirement. - RMD Flexibility

Unlike with Traditional IRAs, you don’t have to take required minimum distributions (RMDs) from a 401(k) if you’re still employed – even after you reach age 73.

- Payroll Deductions

Drawbacks of a 401(k) vs. an IRA Include:

- Limited Investment Options

Most 401(k) plans offer 10–25 funds to choose from, including 1 or 2 international funds. With an IRA, you can invest in virtually any fund you want. - Trickier Communication

Generally speaking, it’s harder to get ahold of a 401(k) representative than a representative through a major IRA custodian like Schwab or Fidelity. - More Barriers to Withdrawals

401(k)s are typically harder to draw from than IRAs; they require more paperwork and a spouse’s sign-off.

- Limited Investment Options

Like IRAs, 401(k)s come in two options: traditional (pre-tax contributions, taxed on withdrawal) and Roth (after-tax contributions, tax-free growth and withdrawals).

2026 Snapshot: 401(k) vs. Other Retirement Plans

| 401(k) | Roth 401(k) | Traditional IRA | Roth IRA | |

|---|---|---|---|---|

| 2026 Employee Contribution Limits (under 50) | $24,500 | $24,500 | $7,500 | $7,500 |

| 2026 Catch-Up Contribution Limits (over 50) | +$8,000* (total $32,500) | +$8,000* (total $32,500) | +$1,100 (total $8,600) | +$1,100 (total $8,600) |

| 2026 Enhanced Catch-Up Contribution Limits (ages 60-63) | +$11,250 (total $35,750) | +$11,250 (total $35,750) | N/A | N/A |

| Tax Treatment | Pre-tax | After-tax | Pre-tax | After-tax |

| Employer Match | Yes | Yes | No | No |

| Required Minimum Distributions (at 73) | No, if still employed | No | Yes | No |

CFP® Tip: You don’t have to choose just one account type. Many people hold multiple account types and move funds between them as circumstances and timelines change.

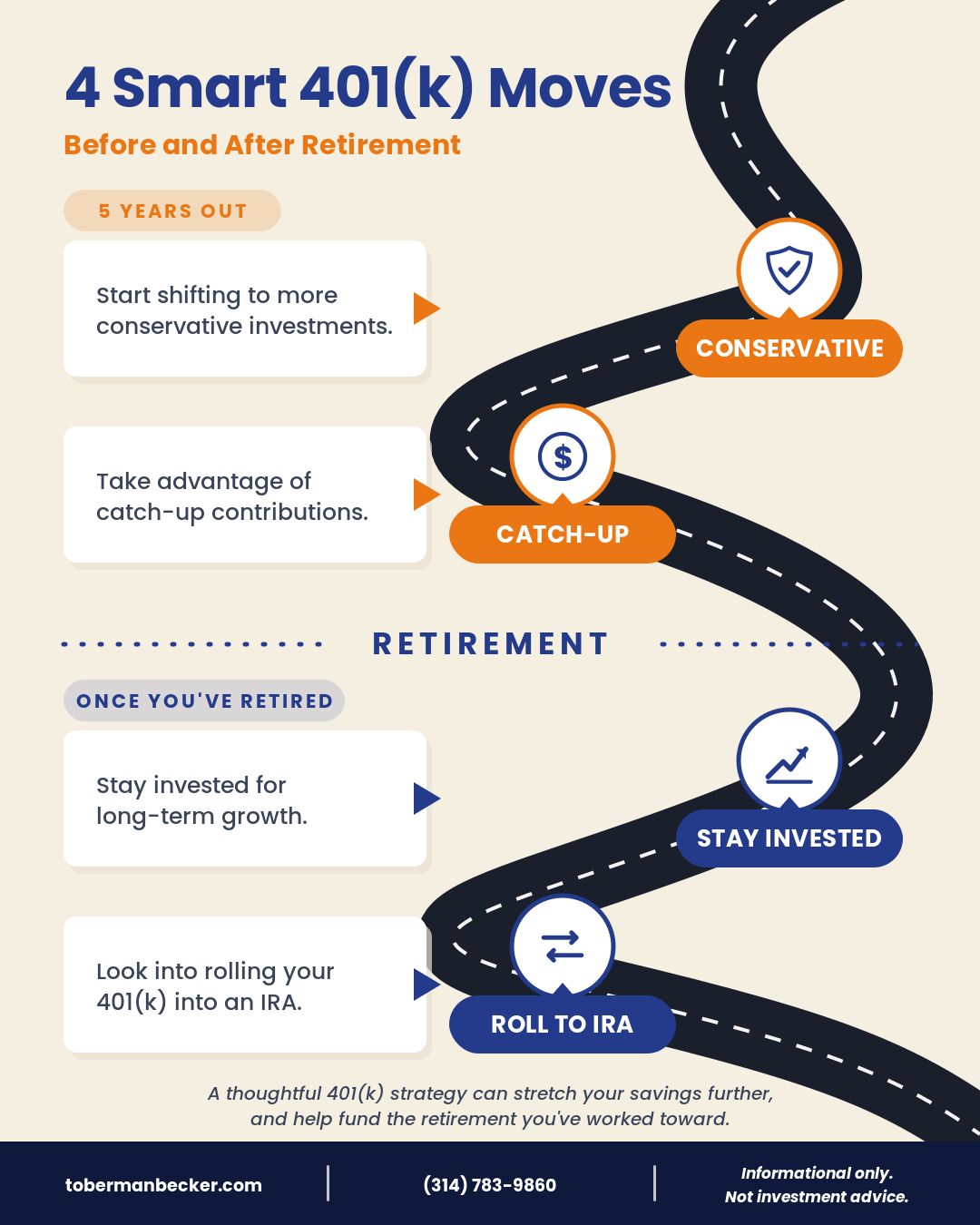

What Should I Do With My 401(k) in the 5 Years Before Retirement?

The five years leading up to retirement are crucial to ensuring your 401(k) supports your long-term financial security. Here’s how to use that time well:

- Assess your cash flow

Determine what your retirement lifestyle will cost, including housing, healthcare, everyday expenses, travel, and hobbies. Once you understand your needs, you can position your portfolio to support them. - Shift your asset allocation

As you approach retirement, your timeline has less tolerance for market fluctuations. Moving some of your investments from stocks to fixed-income products such as bonds can help protect your portfolio from market volatility and prepare it for steady income withdrawals.

CFP® Tip: Aim to have roughly 8 years of living expenses in fixed income or cash equivalents at retirement. Since market cycles average 8 years, this cushion means you can ride out a downturn without being forced to sell stocks at a loss. - Maximize catch-up contributions

If you’re 50 or older and still working, you can contribute more to your 401(k) to increase your available retirement income.

Remember: once you retire, you won’t be able to contribute to your 401(k), so now is the time to take advantage of these catch-up opportunities.

As long as you’re working, you can keep contributing to your 401(k) and are not required to take RMDs. The moment you retire, contributions stop, and you’ll need to decide what to do with what you’ve accumulated.

What Should I Do With My 401(k) After I Retire?

Once you’ve retired, you generally have three options:

- Keep it in your employer’s plan

Your investments continue to grow tax-deferred (traditional) or tax-free (Roth) inside the plan. This option can make sense if your plan has low fees or strong investment options, but remember that 401(k)s can be harder to access than IRAs, and RMDs begin at age 73. - Roll over into another account

This is one of the most commonly recommended moves for retirees. A direct rollover is tax-free and opens up a broader range of investment options. Rolling a traditional 401(k) into a traditional IRA keeps your tax-deferred status; converting to a Roth IRA triggers a one-time tax on the amount moved, but locks in tax-free growth and withdrawals going forward.

CFP® Tip: If you retire before RMD age, consider doing Roth conversions in small batches over 5-10 years. You’ll pay relatively low taxes each year to get it into a Roth bucket, and you’ll gain more control over withdrawals and reduced future RMDs. - Cash out

Cashing out your 401(k) in a lump sum is almost never a good idea. Withdrawals from a 401(k) are taxed as ordinary income, so you pay taxes on the full amount, and you could push yourself into a higher tax bracket that year.

If you’re not sure which option is best for you, a financial advisor can help.

How Can a Financial Advisor Help Me Manage My 401(k)?

A financial advisor can help you integrate your 401(k) management into your broader retirement plan, understanding how it works with Social Security timing, RMDs, tax planning, healthcare, and estate and gift planning considerations. This holistic approach helps your retirement plan support the retirement you want to live for as long as you need it to.

A good advisor will:

- Run a sufficiency analysis: This modeling looks at your full financial picture to determine whether your money will support the lifestyle you want in retirement – for the rest of your life.

- Model rollover and Roth conversion strategies: Identify windows where conversions make the most sense and help you move money between accounts efficiently.

- Build a tax-smart withdrawal plan. Coordinate withdrawals from multiple buckets – 401(k), IRA, Social Security, pensions – to form a smart withdrawal timing strategy that minimizes your tax burden.

A financial advisor can help you feel confident in your retirement plan before you pull the trigger, then act as your partner throughout retirement to keep your plan on track.

Speak With a CFP® Professional About Your 401(k) Before and After Retirement

Whether you’re retirement planning in your 50s or in your 60s – or already enjoying retirement – Toberman Becker Wealth coordinates smart 401(k) decisions to support your dream retirement. See whether your retirement income plan is sustainable by booking a meeting or giving us a call to discuss how we can help.

Mike is a knowledgeable advisor at Toberman Becker Wealth in St. Louis. As a CERTIFIED FINANCIAL PLANNER® professional, he brings strong technical expertise and a client-first approach to helping families build and manage wealth at every stage of life. He prioritizes financial education, empowering clients to make informed decisions.

What sets Mike apart is his commitment to continuous growth. He is always expanding his knowledge to deliver better outcomes for the families he serves and values collaboration with colleagues to improve client experiences. At Toberman Becker Wealth, this commitment to learning and teamwork helps drive exceptional client experiences.

Outside of work, Mike enjoys anything related to golf—spending time with family on the course, competing with friends, and sharing his love for the sport at youth golf camps.